BPR 375: Unbundling of shares in a CFC

SARS has published Binding Private Ruling (“BPR”) 375 which relates to the unbundling of shares in a controlled foreign company (“CFC”).

This ruling determines the tax consequences of an unbundling transaction, in terms of section 46 of the Income Tax Act 58 of 1962 (“IT Act”), of the shares in a controlled foreign company (“CFC”).

The parties to the proposed transaction:

- The applicant: A resident company

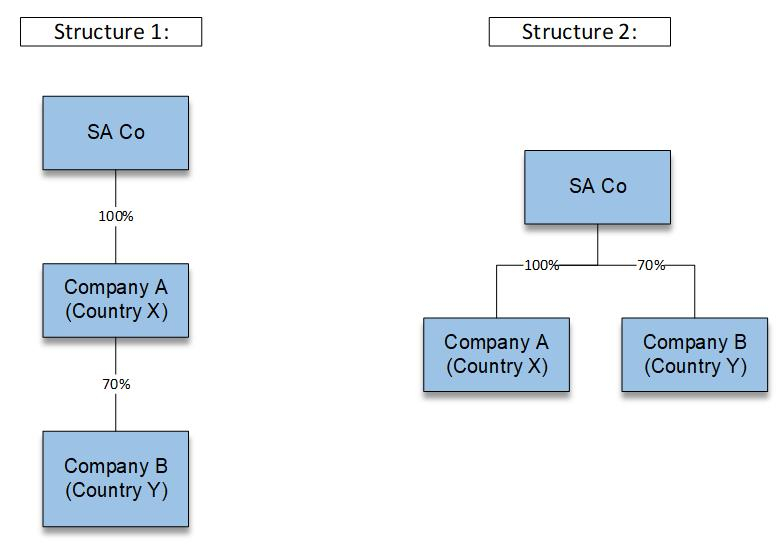

- Company A: A CFC that is a resident of country X and a wholly owned subsidiary of the applicant

- Company B: A CFC that is a resident of country Y and 70 per cent held by Company A

The applicant and its subsidiaries would like to restructure the group as there is no economic benefit for the applicant holding Company B via Company A.

The applicant prefers to exercise direct control over its investment in Company B and the revised structure will place all the applicant’s subsidiaries at the same level without administrative hurdles. The proposed transaction entails Company A unbundling all its shares in Company B to the applicant.

The above transaction has the effect that the group structure changes as follows:

Ruling:

The ruling made in connection with the proposed transaction is as follows:

(a) The proposed distribution by Company A of the shares held in Company B to the applicant will constitute an “unbundling transaction” as defined in paragraph (b) of the definition of that term in section 46(1).

(b) In terms of section 46(2) Company A must disregard the distribution of the shares in Company B for purposes of determining its taxable income or assessed loss or its net income as contemplated in section 9D.

(c) The distribution of the shares by Company A must be disregarded in determining any liability for dividends tax in terms of section 46(5).

Find a copy of the BPR here.

16/08/2022

Contacts