Joint Audit in South Africa

Our goal is to help create a vibrant, innovative audit market that meet the needs of shareholders, broader stakeholders, and wider society. To do this, we must kick-start the creation of a competitive market which encourages new players to take on the audits of listed entities.

What is it?

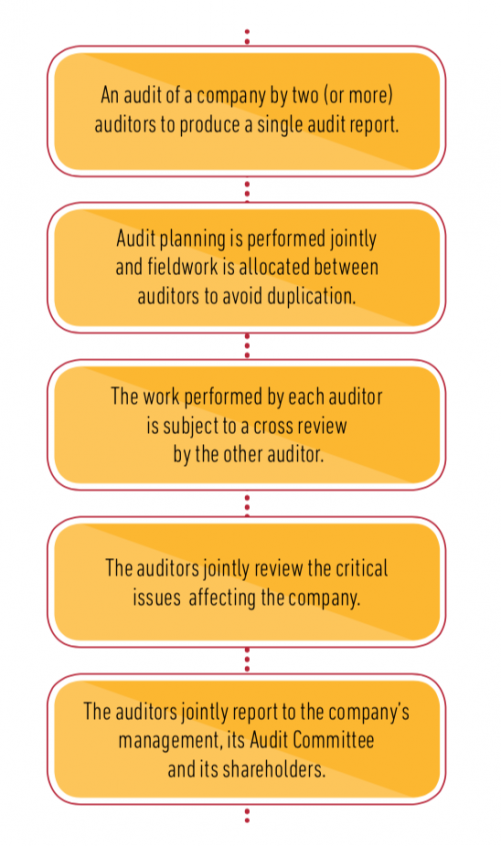

A joint audit is where two separate audit firms are appointed by a company to express a joint opinion on its financial statements.

- It is fundamentally different from a ‘dual’ audit (or ‘shared’ audit) whereby one audit firm (or sometimes more) auditing parts of a group reports to another audit firm that ultimately signs off on the group audit.

- Statutory joint auditors MUST belong to separate audit firms. Joint audits usually involve two audit firms but a small number of companies have decided voluntarily to appoint three audit firms to perform their joint audit.

Why are we talking about it now?

The South African audit sector has been subject to close scrutiny over recent years, thanks in part to high profile corporate failures, as well as an acknowledgment that the market is overwhelmingly concentrated among just four firms.

There are multiple reviews underway globally, each looking at particular elements which affect the industry.

How does it work?

Who uses it?

Joint audit applies in a number of situations:

- Joint audit is mandated in France for all companies required to prepare and publish consolidated financial statements, as and banking entities with total assets in excess of €450m.

- Joint audit is mandated in various countries for large banks or insurance companies, such as in South Africa for large banks.

- Joint audit can be (and is) performed as a voluntary arrangement for groups or even for individual companies, notably across Europe, including in the UK. Joint audit is fully compliant with ISA 600 (Revised), “The Work of Related Auditors and Other Auditors in the Audit of Group Financial Statements”.

For a more detailed analysis, please download our guide below

Want to know more?

Related Pages

Joint Audit: The Facts

In the UK, Joint Audit represents a different and unfamiliar way of approach the audit process. It is also widely misunderstood thanks to a continued focus on decades-old anecdotes based on a limited experience of joint audits undertaken in very different circumstances to those in the present.

CMA Market Review

The Competition and Markets Authority (CMA) has conducted a market review into the state of audit in the UK. As part of this process, it consulted accounting firms, academics, companies and regulators to understand the issues in the sector and to identify opportunities for reform.

Audit & Governance Reform

The release of the BEIS White Paper in March 2021 signalled a once in a generation opportunity to transform audit and strengthen corporate governance in the UK. A consultation followed and the themes were echoed in the transcript of the Queen’s Speech in May 2022. We now await a draft Bill, expected in 2023/4. There is widespread consensus that the audit sector is not reaching its potential, and...