New EU sustainability regulations

The Corporate Sustainability Reporting Directive (CSRD) is the much-anticipated update to the existing Non-Financial Reporting Directive which, in 2014, created reporting and transparency obligations on sustainability matters for a number of European companies, outlined below.

The CSRD widens the scope of companies subject to mandatory sustainability reporting obligations, and aims to improve the quality of reported sustainability information by imposing the mandatory use of European Sustainability Reporting Standards and mandatory audit of sustainability reports produced in compliance with the CSRD.

What has been announced?

On 22 June 2022, The European Council and Parliament, following a long period of political negotiation, reached an agreement on a slightly revised version of the initial CSRD proposal made by the European Commission in April 2021 (a link to our 2021 publication can be found below in the How can I learn more? section). Here are the links to the recent Parliament and Council press releases.

The final text has yet to be made public within a few days or weeks, and particular attention will need to be paid to the detail of the final provisions. Here are the highlights you need to know about today.

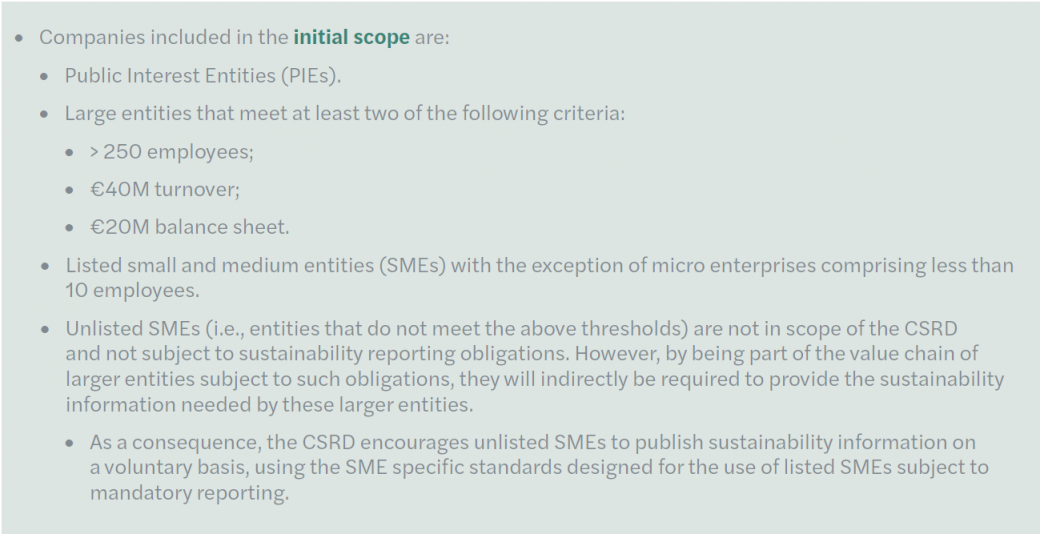

All initial key features of the CSRD proposal are confirmed:

A few key points on aspects that have been introduced:

How can I learn more?

There is a variety of ways to understand more about the CSRD, which is as follows:

• Read this Mazars publication on the CSRD.

• Listen to this podcast on the transition towards the CSRD.

• Explore existing Mazars publications on the CSRD and Taxonomy – contact us for more information.