The growing divide between Treasury's expectations and SARS results

On 1 April 2019, the South African Revenue Service (SARS) reported its preliminary results, which exposed a revenue collection shortfall of approximately R14.6 billion for the 2018/19 financial year. As many have been quick to point out, this makes it the fifth consecutive year that the organisation has missed its collection targets.

However, what is not immediately clear from the numbers above, is the fact that there seems to be a growing disparity between Treasury’ projections with regards to tax revenue collection at the start of each financial year and SARS’ ability to meet those targets.

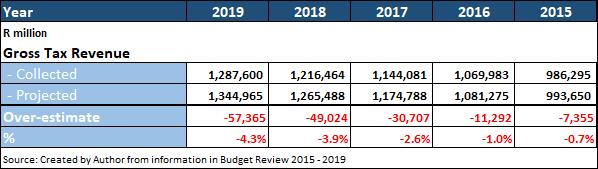

While revenue collection isR14.6 billion short of the revised R1.302-trillion target set during the 2019 Budget Speech in February, SARS actually missed the collection target set during the 2018 Budget Speech in February of last year by substantially more. Revenue collection is, in fact, R57.4 billion less than Treasury’s initial target of R1.345-trillion.

Considering the collection results compared to the original estimates made one year prior to the actual results, one can clearly see how quickly this disparity has grown. The financial year ending 31 March 2015 saw SARS fall short by 0.7% of the initial target (R7.355 billion). This percentage has been steadily increasing over the past five years jumping to 3.9% (R49.024 billion) in 2018, and peaking in the current financial year at over 4% (R57.365 billion).

Whilst SARS is in the process of making many positive changes to improve its ability to collect outstanding tax revenue, the projected revenue for the 2019/20 financial year leads one to wonder if Treasury is consistently setting an unachievable target for SARS.

Treasury’s projection for tax revenue in 2020 is R1.422 trillion, which is 10.5% higher than the actual taxes raised in 2019.

This prediction seems overly optimistic in light of the fact that the World Bank recently cut its growth forecast for South Africa for 2019 from 1.8% to 1.3%. Furthermore, the 2019/20 Budget did not put forward any interventions conducive to stimulating economic growth in the country, having not introduced much in the way of tax incentives that could help grow employment and, by extension, the taxpayer base.

As usual, the bulk of the tax revenue that SARS aims to collect is expected to come from corporate and personal income taxes, which may also prove problematic in terms of its targets. During the 2019 Budget Speech, Treasury announced that it would raise additional revenue from personal income tax to the tune of around R12.8 billion by not adjusting tax brackets and relying on fiscal drag to do the rest.

However, this assumes that taxpayers will receive inflationary or above-inflationary salary increases this year. In a poorly performing economy, there are few guarantees that this would happen. The taxable income for corporates will also likely suffer some blows if the economy continues on its current trajectory.

Tax filing compliance in South Africa has also seen a downturn, which is once again pointing to the fact that taxes in the country have reached their limit and that further tax increases are likely to see revenue collections decrease. According to SARS, filing compliance with regards to PAYE slipped from 83.9% in 2008/09 to 68.9% in 2018/19. Filing compliance with respect to VAT dropped from 79% to 61.7% over the same period.

While there is undoubtedly some light at the end of the tunnel for SARS with its renewed focus on efficiency and the recent appointment of its new commissioner, there are no real guarantees that the organisation will be able to turn the current situation around within the next year or two.

As the newly appointed SARS commissioner-designate Edward Kieswetter recently stated, for the organisation to advance, it will be crucial to be plugged into the economy and to understand what is happening. Perhaps the best starting point would be to take a long hard look at the goals being set for the organisation and asking whether the optimism displayed in the current revenue collection target is realistic.

Author: Tertius Troost.

Tertius